Pavel Babic

We previously covered First Solar, Inc. (NASDAQ:FSLR) in January 2024, discussing how its utility-scale solar panels remained in hot demand, with its growing backlog extended through 2030 at favorable ASPs.

Combined with the bottomed solar investment thesis and the normalizing macroeconomic outlook, we maintained our Buy rating for the stock then.

In this article, we shall discuss why we are maintaining our optimistic view surrounding FSLR’s cadmium telluride investment thesis, despite the intensified pricing competition from Chinese-produced silicon-based solar panels and the former’s decelerating backlog growth.

With the stock already charting an impressive +13.5% price return since our previous article, we believe that the stock remains well positioned to more than double from current levels, with the management prudently sizing their investments and capacity expansions.

Interested investors may add at any dips.

The FSLR Investment Thesis Remains Robust

For now, FSLR has reported a bottom-line beat in the FQ4’23 earnings call on February 27, 2024, with net sales of $1.15B (+43.7% QoQ/ +15.6% YoY) and EPS of $3.25 (+30% QoQ/ +4742.8% YoY), and FY2023 numbers of $3.31B (+26.7% YoY) and $7.74 (+1987.8% YoY), respectively.

The growing bottom line is naturally attributed to the solar company’s ability to deliver on its historic backlog of 80.1 GWs and a global opportunity pipeline of 66.5 GWs as of FQ4’23, thanks to the drastic expansion in its nameplate capacity to 16.6 GWs by the end of the year (+69.3% YoY) at favorable ASPs.

As a result, it is unsurprising that the management has offered an excellent FY2024 revenue guidance of $4.5B (+35.9% YoY) and EPS guidance of $13.50 (+74.4% YoY) at the midpoint, with sales volumes of 15.95 GWs (+39.9% YoY).

Most importantly, the management has been able to deliver these numbers with a relatively healthy balance sheet at a net cash situation of $1.63B (+20.7% QoQ/ -31.7% YoY) by FQ4’23, despite the intensified FY2023 capex of $1.38B (+53.4% YoY).

Inherent Risks From Silicon-Based Solar Panel Producers

Utility Scale PV Installations In The US By Module Type

Berkley Lab

Then again, the FSLR investment thesis is not all roses as well, given that silicon-based solar panel remains the most popular choice for utility-scale energy producers, comprising 62% of the newly installed capacity in the US compared to 38% for thin-film modules in 2022, based on the latest data released by Berkley Lab in 2023.

While LONGi, Canadian Solar, and Hanwha may lead in terms of silicon market share at approximately 15% of the 2022 silicon installation, it is apparent that 52% of the silicon installations come from unknown origins.

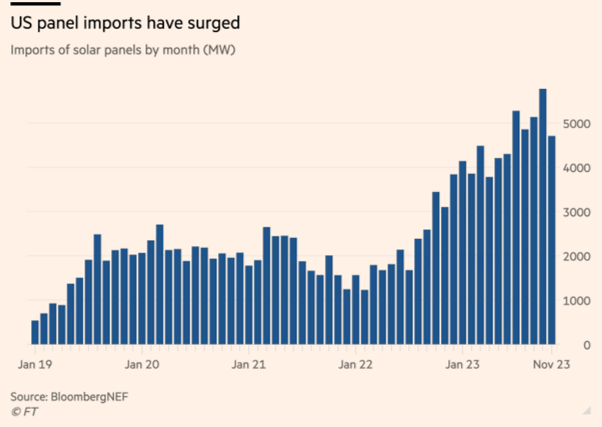

Surging US Import Of Solar Panels

BloombergNEF, Financial Times

The FSLR’s CEO has already suggested that the influx of Chinese-produced solar panels may overwhelm the domestic solar market while crippling domestic suppliers, attributed to the improved affordability with “US power companies favoring imports over the more expensive domestic panels.“

Low-Priced Chinese-Produced Solar Panels & Sustained Expansion In Capacity

Wood Mackenzie, PV Magazine, BloombergNEF, Financial Times

This is unsurprising, since Chinese-produced solar panels typically cost less than 11 cents per watt, compared to Southeast Asian panels with Southeast Asian cells at less than 16 cents per watt, US panels with Southeast Asian cells at less than 16 cents per watt, US panels with US cell at less than 19 cents per watt, based on data from BloombergNEF.

Readers must also note that FSLR reports FQ4’23 bookings with a base ASP of 31.8 cents per watt, or 33.4 cents per watt including contract technology adjusters, further exemplifying why cheaper Chinese-produced silicon panels have been more popular.

Combined with the sustained capacity expansion by multiple silicon producers in China, it is unsurprising that Wood Mackenzie has projected that the country may continue to lead in the global module manufacturing share over the next few years, naturally triggering a sustained price headwind for US-based module producers, FSLR included.

As a result, while FSLR may report a historic backlog while effectively ensuring its top/ bottom line growth through the end of this decade, it remains to be seen how the overall solar market may perform moving forward.

At the same time, readers must note that market analysts already expect solar panel prices to further decline in the US, from 23 cents per watt in 2024 to 16 cents per watt by the end of 2025, with the 2022 Inflation Reduction Act’s subsidy of 7 cents per watt unlikely to be sufficient.

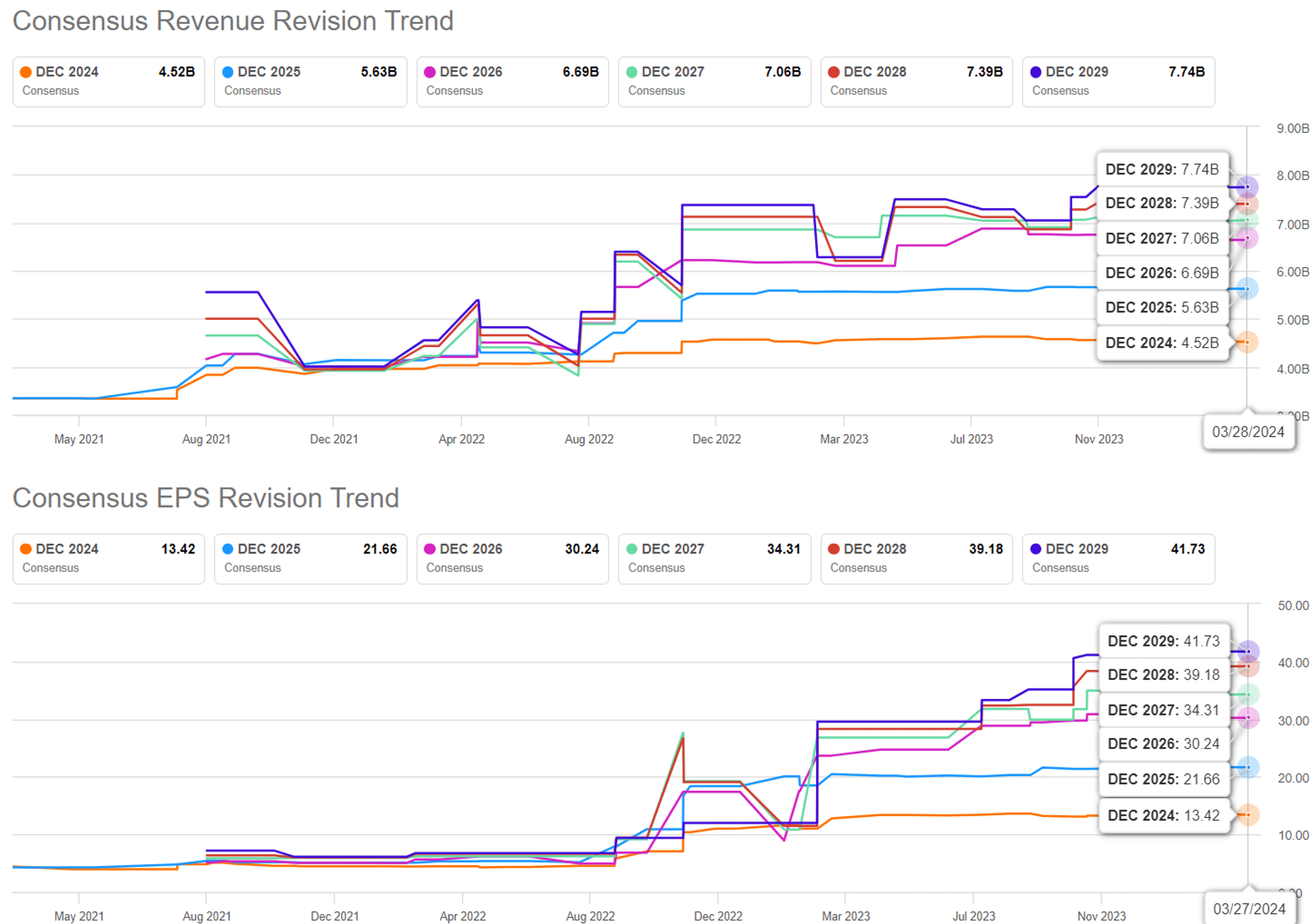

The Consensus Forward Estimates

Seeking Alpha

Therefore, while FSLR is expected to generate a robust top/ bottom line growth at a CAGR of +15.2%/ +31.5% through FY2029, raised from the previous estimates of +13.4%/ +27.8%, readers may also want to temper their expectations.

This is especially true since the management has reported certain “requests from customers to shift delivery volume timing out as a function of project development delays” in the recent FQ4’23 earnings call, likely to trigger headwinds to its long-term investment thesis as the backlog growth decelerates.

For context, FSLR reports FQ4’23 net bookings of 2.3 GWs (-66.1% QoQ/ -80.8% YoY) and FY2023 net bookings of 28.3 GWs (-41.4% YoY), with a flattish base ASP of approximately 0.30 cents per watt.

With the solar company already reporting a fully booked backlog through 2026 and staggered delivery through 2030, we believe that it is prudent to expect decelerating double-digit growth ahead as more of its nameplate capacity comes online over the next few years.

So, Is FSLR Stock A Buy, Sell, or Hold?

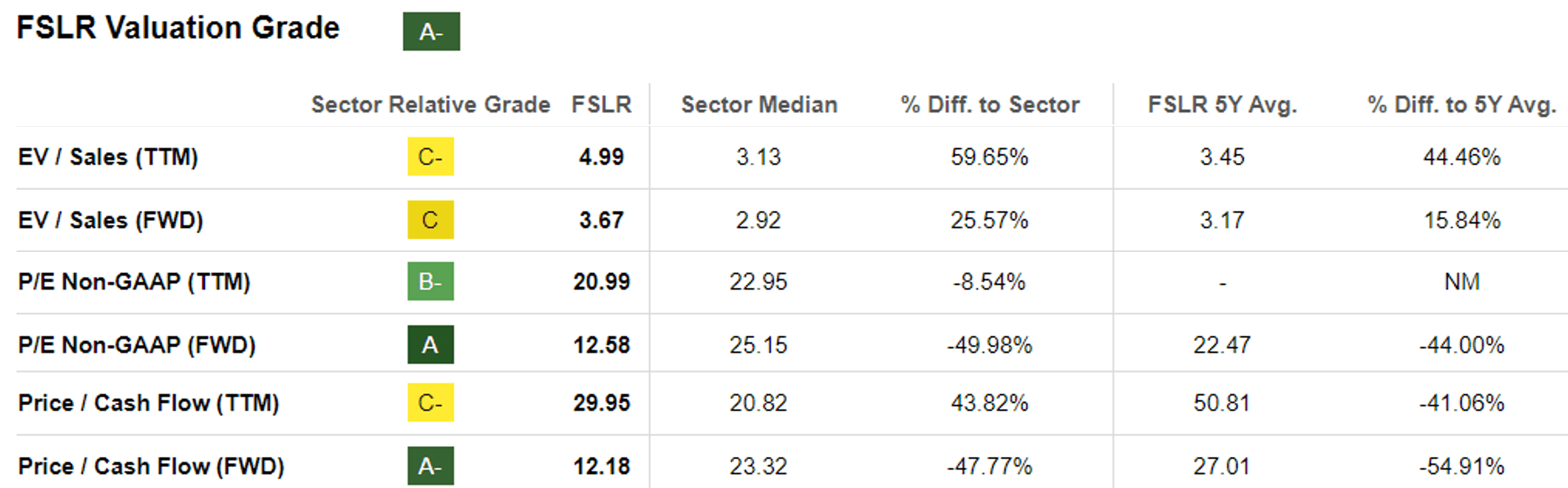

FSLR Valuations

Seeking Alpha

As a result, it is unsurprising that the market has temporarily discounted FSLR’s valuations to FWD P/E of 12.58x and FWD Price/ Cash Flow of 12.18x, compared to the previous article at 20.25x/ 17.28x, its 5Y mean of 22.47x/ 27.01x and sector median of 25.15x/ 23.32x, respectively.

Even then, it appears that market sentiments have turned away from solar producers, with its peers trading at impacted valuations, including LONGi at 11.75x/ NA and Canadian Solar Inc. (CSIQ) at 6.82x/ 1.87x, with renewable energies increasingly priced nearer to utility stocks instead of technology stocks.

FSLR 1Y Stock Price

TradingView

As a result, we can understand why FSLR has been trading sideways after the dramatic pullback in 2023, with the stock also trading above our fair value estimate of $97.30, based on the FY2023 adj EPS of $7.74 and the FWD P/E of 12.58x.

Then again, based on the consensus FY2026 adj EPS estimates of $30.24 and a similar FWD P/E, there seems to be an extremely bullish doubling potential to our long-term price target of $380.40.

This is attributed to its fully booked backlog through 2026, with parts stretching through 2030 at favorable ASPs and price adjusters, as FSLR continues to ramp up its global nameplate capacity to over 21 GWs by 2024 and over 25 GWs by 2026.

Combined with the more efficient labor costs in the new plants in India, Vietnam, and Malaysia, we believe that the consensus FY2026 EPS estimates are not overly ambitious indeed, due to the prospective improvements in its global operating scale.

In addition, while there may be intensified domestic silicon manufacturing competition from LONGi in Ohio, Hanwha Qcells in Georgia, and CSIQ in Texas from 2023 onwards, putting further pressure on FSLR’s backlog growth, we believe in the latter’s Cadmium Telluride solar technology.

For example, FSLR has recently achieved a world record Cadmium Telluride in-lab conversion efficiency of 22.6% by 2023 and module efficiency of 19.7% in 2022, with the management targeting a module efficiency of 28% by 2030 compared to the theoretical limit up to 35.79%.

This is compared to the current silicon-based module efficiency of over 25% and the theoretical limit of 29.4%.

This is on top of FSLR’s launch of the first bifacial thin film Cadmium Telluride solar panel, with the new technology expected to generate a higher energy yield by up to +23% than the monofacial or single-sided counterparts.

Lastly, the management also confidently reiterates a 0.2% degradation rate with the CuRe technology set to launch in 2024, compared to the 0.6% reported for silicon-based solar panels, effectively improving the long-term stability and performance.

If anything, we expect thin-film Cadmium Telluride-based solar panels to gain in adoption, with it typically being able to withstand extreme weather conditions, such as hailstorms, which has recently damaged thousands of silicon-based solar panels in the Fighting Jays Solar Farm in Texas.

Combined with the geopolitically secure supply chain, FSLR’s cadmium telluride recycling program, and insignificant leaching/ fire risks during extreme conditions, we believe that utility demand may remain robust moving forward, despite the inherent risks from silicon-based solar panel producers as discussed above.

As a result of the long-term electrification trend, the expanded manufacturing capacity, and the decade-long backlog, we are maintaining our Buy rating for the FSLR stock.

This post was originally published on 3rd party site mentioned in the title of this site